Market Snapshot

Launching In Vivo’s oncology therapeutic review series, this first instalment provides a data-led primer on the global cancer landscape. Future instalments will explore market dynamics, pipeline evolution and the innovations set to define oncology therapeutics through 2032.

Cell and gene therapy is shifting into a new phase, as maturing commercial launches, rising big pharma participation and regulatory momentum replace hype and skepticism.

Sun launches tildrakizumab, its star psoriasis therapy in India seven years after US FDA approval at what’s seen as a carefully calibrated price point. Can it ruffle entrenched products like secukinumab?

Leaders from Eli Lilly, Novo Nordisk, Biocon, Dr Reddy’s and Levim discuss the huge India market potential for GLP-1s. Executives from the Indian firms also outlined efforts to build supply chain stability and cost-efficiency for products like semaglutide.

Glioblastoma carries a grim prognosis. The biopharma industry is trying to improve patient outcomes, with 120 drugs in the pipeline and two anticipated approvals this year.

More BCMA-directed therapies are in development, as well as ones targeting GPRC5D and FcRH5, along with CELMoDs. The question is how to bring those into therapy and pay for them.

KOLs told Scrip about how they are incorporating new immunotherapies into treatment and combining existing agents, but some new drug classes have struggled to take root.

The recent US approval of Ferring’s microbiome-targeting Rebyota is set to change the treatment landscape for recurrent Clostridioides difficile infection and could be the proving ground for this class of agents. Rebyota is the first microbiome-targeting treatment to reach the market, but several promising candidates for the same indication are waiting in the wings.

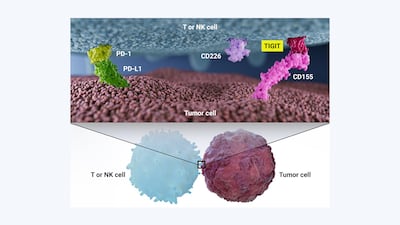

The promise of TIGIT as an oncology target in combination with PD-1/PD-L1 inhibitors has prompted an influx of investment into anti-TIGIT agents and five agents are already in advanced clinical trials. That initial enthusiasm has been dampened as of late, after disappointing Phase III data. Investors are hoping that 2023 will be the year that restores hope in the anti-TIGIT pipeline.

Multi-product players may be able to use bundled rebates for preferred formulary status and biosimilars offer a new competitive dynamic, but there is hope for novel therapies.

Remission rates with existing therapies leave much room for improvement, so a variety of treatments are needed – leaving major players attempting to carve unique paths in a crowded market.

The ulcerative colitis and Crohn’s disease landscapes may shift soon but new drugs will compete with entrenched blockbusters, including Humira, Stelara and Entyvio, with biosimilars on the way.